Fair Isaac Corporation (FICO) Score Cross-Sectional Analysis of United States Surgeons and Anesthesiologists

by Peter Palumbo1,2, Jamal J Hasoon3, Paul J. Christo4, Melissa Murphy5, Timothy Flanagan6, Omar Viswanath7,8, R. Jason Yong9*, Wael Saasouh10,11#, Christopher L. Robinson4*#

1Geisel School of Medicine at Dartmouth, Hanover, NH, USA

2The Tuck School of Business at Dartmouth, Hanover, NH, USA

3Department of Anesthesia and Pain Medicine, UTHealth McGovern Medical School, Houston, TX, USA

4Division of Pain Medicine, Department of Anesthesiology and Critical Care, The Johns Hopkins University School of Medicine, Baltimore, MD, USA

5North Texas Orthopedics and Spine Center, Grapevine, TX, USA

6Spencer Fox Eccles School of Medicine, University of Utah, Salt Lake City, UT, USA

7Mountain View Headache and Spine Institute, Phoenix, AZ, USA

8Department of Anesthesiology, Creighton University School of Medicine, Phoenix, AZ, USA

9Department of Anesthesiology, Perioperative and Pain Medicine, Brigham and Women’s Hospital, Boston, MA, USA

10Department of Anesthesiology, Wayne State University, Detroit, MI, USA

11Outcomes Research Consortium®, Houston, TX, USA

#Denotes equal contribution.

*Corresponding Author: Christopher L. Robinson, Department of Anesthesiology and Critical Care, Division of Pain Medicine, The Johns Hopkins University School of Medicine, Baltimore, MD, USA

Received Date: 20 April 2026

Accepted Date: 27 April 2026

Published Date: 29 April 2026

Citation: Palumbo P, Hasoon JJ, Christo PJ, Murphy M, Flanagan T, et al. (2026) Fair Isaac Corporation (FICO) Score Cross-Sectional Analysis of United States Surgeons and Anesthesiologists. J Surg 11: 11615 DOI: https://doi.org/10.29011/2575-9760.011615

Abstract

Physician finances are recognized as an important component of physician wellness with implications for workforce distribution and public health. Although physician income by specialty is well documented, limited data characterize the financial standing of surgeons and anesthesiologists. Credit scores provide an objective marker of financial stability and access to capital. The Fair Isaac Corporation (FICO) score, ranging from 300–850 and derived from credit bureau data, is widely used by lenders to evaluate creditworthiness. This cross-sectional study analyzed pooled FICO scores from 522 U.S. surgeons and 293 U.S. anesthesiology borrowers who applied for personal loans between 2019 and 2023 through Doc2Doc Lending. Variables included FICO score, training status (trainee vs attending), CDC-defined geographic region, and loan purpose. The overall median FICO score was 698. Surgical trainees (n=323) had a median score of 681 (IQR 645–724), while surgical attendings (n=199) had a median of 723 (IQR 679–791), a 42-point difference (p<0.0001). Anesthesia trainees (n=147) had a median score of 690 (IQR 657–734), while attendings (n=146) had a median of 724 (IQR 683–772), a 34-point difference (p<0.0001). Surgical trainees most commonly borrowed for credit card consolidation, relocation, and other expenses, and surgical attendings most often borrowed for credit card consolidation, other expenses and home improvement. Anesthesia trainees most commonly borrowed for credit card consolidation, relocation, and other expenses, whereas anesthesia attendings most often borrowed for home improvement, credit card consolidation, and debt refinancing. Borrowing patterns differed by training stage, suggesting changing financial priorities across career progression.

Keywords: Cross-Sectional Analysis; Debt; Fico; Physician; Trainees

Key Summary Points

- Physician financial wellness has important implications for public health and workforce stability, yet objective data characterizing physicians’ financial health beyond income are limited, particularly during training.

- Credit scores serve as a proxy for financial wellness and access to capital and may reveal persistent financial strain among physicians despite high long-term earning potential.

- The study asked whether U.S. Surgeons and Anesthesiologists credit profiles differ by training status, specialty, geography, and borrowing reason, and whether credit scores improve after entering independent practice.

- Among 522 surgeon and 293 anesthesiologist borrowers, attending physicians had significantly higher median FICO scores than trainees in both groups (723 vs 681 and 724 vs 690 respectively), slightly above the U.S. national average of 718.

- Credit card debt consolidation was the most common reason for loan applications among both surgical and anesthesia careers, highlighting ongoing financial strain early in physicians’ careers.

Introduction

Physician finance is a frequently discussed component in conversations of physician wellness with broader public health implications. Student debt, for example, has been shown to impact decisions surrounding specialty and willingness to practice in underserved areas [1]. While annual reports exist outlying physician income by specialty, no further data characterizes the state of surgeons and anesthesiologists’ finances [2,3]. Credit scores provide a useful marker for identifying the likelihood to pay back a loan but also serve as a proxy for financial wellness and access to capital. The Fair Isaac Corporation (FICO) score is a three-digit, mathematically-derived number from 300 to 850 incorporating data from the three credit bureaus (Equifax, Experian, and Transunion) [4,5]. The FICO score is a widely used metric that utilizes factors such as outstanding debt and payment history to suggest a prospective borrower’s ability to repay debt [4]. For individuals living in the US, this becomes a metric against which loan applications are decided, especially for important purchases such as a home mortgage. The FICO score excludes age, employment history, gender, location, income, marital status, national origin, and race to protect customers from potentially discriminatory credit decisioning [5].

Methods

This cross-sectional study is based on pooled FICO scores from 522 U.S. surgeon and 293 U.S. anesthesiology borrowers who applied for loans from 2019 to 2023. The data were sourced from Doc2Doc Lending (Atlanta, Georgia, USA), a privately held financial services company for physicians and dentists that operates in compliance with the Equal Credit Opportunity Act. Variables included individual FICO scores, training status (trainee vs attending), geographical regions as defined by the CDC, and reasons for the loan (Table 1 and Figure 1). Trainees were defined as those who applied and accepted a loan within the time between obtaining a residency position as fourth year medical students and completion of residency or fellowship training. The distribution of the trainee and attending physician credit scores were initially analyzed for normality based on a multiple linear regression model and the residuals were assessed by the Kolmogorov-Smirnov test. Since each population was found to have a non-normal distribution, medians and Interquartile Ranges (IQR) were reported and compared using the Mann-Whitney U test. Further ethics committee approval was not required as this was a descriptive secondary analysis of data that was previously collected for other purposes.

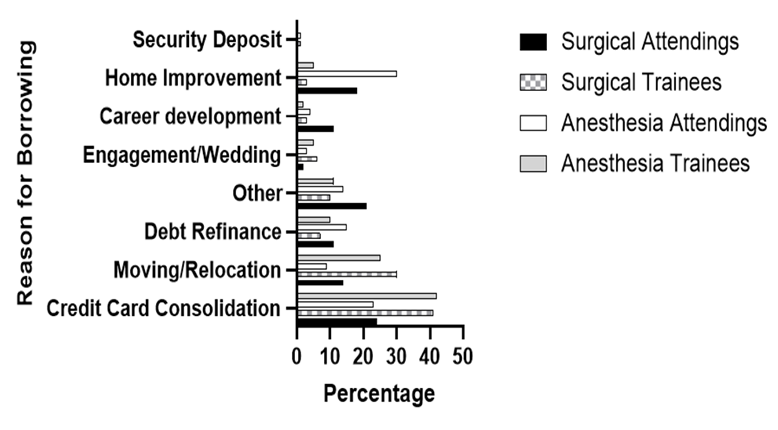

Figure 1: Reasons for acquiring the loan. (Surgical Trainees n = 323, Attendings n = 199, Anesthesia Trainees n = 147, Attendings n = 146).

|

Surgeons |

|||

|

Attendings |

Trainees |

p-values |

|

|

Number |

199 |

323 |

- |

|

Median FICO score |

723 |

681 |

< 0.0001 |

|

FICO Categories (n) |

|||

|

Poor (300-579) |

0 |

2 |

< 0.0001 |

|

Fair (580-669) |

38 |

138 |

|

|

Good (670-739) |

82 |

120 |

|

|

Very Good (740-799) |

40 |

60 |

|

|

Excellent (800-850) |

39 |

3 |

|

|

Geographic Distribution Median FICO Scores (n) |

|||

|

Midwest |

723 (39) |

686 (78) |

ns |

|

Northeast |

696 (41) |

683 (97) |

ns |

|

South |

723 (77) |

674 (108) |

< 0.0001 |

|

West |

742 (41) |

672 (40) |

< 0.0001 |

|

Anesthesiologists |

|||

|

Number |

146 |

147 |

- |

|

Median FICO Score |

724 |

690 |

< 0.0001 |

|

FICO Categories (n) |

|||

|

Poor (300-579) |

1 |

0 |

< 0.0001 |

|

Fair (580-669) |

26 |

54 |

|

|

Good (670-739) |

58 |

58 |

|

|

Very Good (740-799) |

39 |

33 |

|

|

Excellent (800-850) |

22 |

2 |

|

|

Geographic Distribution Median FICO Scores (n) |

|||

|

Midwest |

733 (17) |

676 (33) |

ns |

|

Northeast |

710 (29) |

686 (56) |

ns |

|

South |

736 (70) |

696 (28) |

ns |

|

West |

712 (30) |

708 (30) |

ns |

Table 1: Physician borrower comparison between trainees and attendings. Categories include median FICO scores, frequency distribution of FICO score categories, and median geographic distribution. Categories include Poor (300-579), Fair (580-669), Good (670-739), Very Good (740-799), and Exceptional (800-850). Categories include surgeons and anesthesiologists.

Results

We found that among the 815 physician burrowers, the median FICO score was 698 [IQR = 659, 751]. For the 323 surgeon trainees and 199 attendings, the median was 681 [IQR = 645, 724] and 723 [IQR 679, 791] with a difference of 42 points (p < 0.0001) (Table 1). For the 147 anesthesia trainees and 146 attendings, the median was 690 [IQR = 657, 734] and 724 [IQR 683, 772] with a difference of 34 points (p < 0.0001). We also observed no significant difference between the surgeons and anesthesiologists. The distribution of median FICO scores based on categories was skewed to the left for trainees and to the right for attendings. Subgroup analysis by CDC designated geographic regions demonstrated significant differences between surgical attendings and trainees in the South and West (Table 1). The top three most common reasons for loan application among surgical trainees was credit card consolidation (41%, 131/323) followed by moving/relocation (30%, 97/323) and other (10%, 32/323) (Figure 1). For surgical attendings, the most common reasons for borrowing were credit card consolidation (24%, 47/199) followed by other expenses (21%, 41/199) and home improvement (18%, 35/199). Anesthesia trainees also primarily borrowed for credit card consolidation (42%, 62/147), relocation (25%, 37/147) and other expenses (11%, 16/147). Attendings differed, borrowing mostly for home improvement (30% 44/146), but also credit card consolidation (23%, 34/146) and debt refinancing (15%, 22/146). In this cross-sectional study of physicians who obtained personal loans from a financial services company, we found that both trainee and attending physicians had good credit scores despite their student debt and relatively low salaries for trainees. The difference in the top reason for borrowing between anesthesia attendings and trainees, home improvement versus credit card consolidation, may reflect differences in their financial focus by life stage. Whereas the anesthesia trainee may seek to cover necessary expenses, the anesthesiology attending may be able to focus on longer term personal and financial goals. This is not absolute, however. When combined, 47% of anesthesia attendings and 49% of surgical attendings were still borrowing money for the purposes of either debt refinance, credit card consolidation, or moving/relocation.

Limitations

This study is exploratory in nature and does not permit interpretation of causal mechanisms. The study is further limited as the data consists of physician-borrowers applying for a personal loan through a single lender, leading to a selection bias that does not permit generalization of the study’s findings to the general physician population. However, the insight remains unique as this type of data is not typically publicly available. A lack of data available on socioeconomic factors and financial support systems of the borrowers further makes it difficult to characterize the nature of the selection bias.

Conclusions

Interestingly, the median FICO scores of surgical and anesthesia attending borrowers are only eight and nine points higher than that of the average American (715), respectively, despite the attending salary being nearly seven times greater than the average American citizen [2,6,7]. A recent survey of 2,212 students from 91 countries found that 69% of medical students were concerned about their income as an attending [8,9]. Alarmingly, 25% of current US medical students were considering quitting training with 69% stating concern for their financial future [8,9].In the year after New York University began offering tuition-free medical school, applications rose 47%, with a nearly 50% jump in underrepresented minorities who often come from financially disadvantaged backgroundsb [10]. Our findings that trainees and attendings alike are seeking personal loans to cover credit card debt and costs of relocation validate the concerns of U.S. medical students and offer a glimpse into what some of the benefits of tuition-free medical education might be. This dovetails with new caps on student borrowing which will force students to seek funding in the private market, and constant threats to many student loan programs that are uniquely favorable to the prolonged physician training timeline – income driven repayment and public service loan forgiveness. The prospect of increasing a source of financial stress may be reflected in their FICO scores in the years to come with burnout and exit rates as a further downstream consequence of greater burden in the crucial residency period.

Declaration of Interests

Acknowledgements: Funding was provided by Doc2Doc Lending.

Conflicts of Interest: CR, PP, WS, JY are consultants for Doc2Doc Lending.

Author Contributions: PP, RJY, WS, and CLR devised, analyzed, and wrote the paper. JJH, PJC, MM, TF, OV, CW, ABJ assisted with writing, revising, and providing expertise.

Ethics/Ethical Approval: Ethics committee approval was not required for this study as it did not involve patients and all data was de-identified.

References

- Rohlfing J, Navarro R, Maniya OZ, Hughes BD, Rogalsky DK (2014) Medical student debt and major life choices other than specialty. Med Educ Online 19.

- Doximity 2024 Physician Compensation Report.

- (2023) Physician Compensation Report.

- (2025) What Is a FICO Score?).

- Doroghazi RM (2020) FICO Scores. Am J Cardiol 130: 157-158.

- Average US FICO Score Drops to 715 | FICO.

- (2025) National Average Wage Index.

- 1 in 4 US medical students consider quitting, most don’t plan to treat patients: report.

- (2025) Clinician of the Future 2023 Education Edition.

- (2025) MarketWatch.

© by the Authors & Gavin Publishers. This is an Open Access Journal Article Published Under Attribution-Share Alike CC BY-SA: Creative Commons Attribution-Share Alike 4.0 International License. Read More About Open Access Policy.